Individual Futures Options Solutions

Tận dụng các tính năng của quyền chọn tương lai mà không cần phải sử dụng các công thức toán học phức tạp.

Chúng tôi cung cấp nhiều loại giải pháp khác nhau.

Trong mỗi danh mục, chỉ có một số ít giải pháp được cung cấp, chủ yếu nhằm mục đích minh họa ý tưởng. Số lượng các giải pháp tùy chọn khả thi thực tế là không giới hạn.

Global rates have risen. Many banks do not pay comparable interest on deposits. To get a good rate on a deposit, it is usually necessary to choose a long term without the possibility of withdrawing the deposit. Many futures brokers do not pay interest on balances or pay a disproportionate rate.

Solution.Certain option solutions provide fixed returns comparable to current market rate.

In this case:

There is a forecast of changes in prices for an asset over a certain horizon. There is a choice of options solutions on how to work out the forecast. But these solutions are not free, but require the payment of option premiums.

Solution.The right combination of the strategies in Solution 1 and the options solutions provide a “free” solution that offsets the payment of option premiums.

There is a forecast of quite strong movement for the day.

Solution.A today's option (with an expiration date today) is purchased in the hope that the forecast will come true. In this case, profits can be achieved that are multiples of the premium spent.

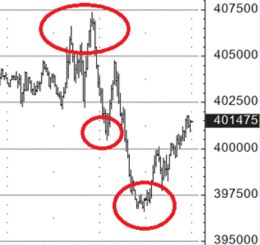

E-Mini S&P 500 futures.

In the area of the top there was a purchase of today's (with expiration today) put with a strike of 4000 for 1.00 points ($50). In the first “poke” down, the option cost 20.00 points ($1,000), that is 20-times of premium paid were made. At the beginning of the second “poke” down, the option cost 34.00 points ($1,700), i.e made 34-times of premium paid.

There is an opinion that it is necessary to limit losses by placing stop orders, the so-called “stop loss”. In this case, the stop order may be executed, but the market then turns in the direction of the original position, which, in the end, could even be profitable.

Solution.Using options as an alternative to stop loss. A stop loss implemented in this way gives the position a greater chance of returning to the profitable zone and eliminates losses associated with gaps beyond the stop loss level.

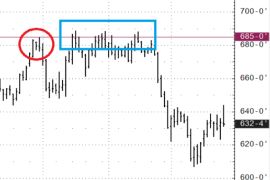

"Stop Loss". Corn futures.

There is a short position in a futures (sold futures). The stop loss level was chosen above the high of 685-0 (red circle). If there was a stop order at 685-0, it would have been triggered (blue area). At the same time, in the end, the market fell and would have brought profit. But the trader was left without a position. Buying a call option with a strike price of 685-0 with sufficient time until expiration would guarantee protection above the 685-0 level, while leaving the position open to profit in the event of a fall. The trade-off for staying in the position is paying an option premium, which would increase losses above the 685-0 level if the market closed above that level on the expiration date.

"Gap". Oil futures.

There is a short position in a futures (sold futures). The stop order is at 76.00, limiting potential losses. However, significant news came out over the weekend and the market opened with a “gap” and the stop order was executed at a price of 80.10, realizing additional losses. If, instead of a stop order at 76.00, a call option with a strike price of 76.00 had been purchased, it would have guaranteed the position to be closed at 76.00. In this case, the maximum additional loss would be limited only by the option premium, which would be significantly better compared to an executed stop order at a price of 80.10. Moreover, since using an option as a “stop loss” there is no need to close the position, there was still a chance (if there was enough time before the option expiration) to wait for the fall and realize the profit as a result.

There is a forecast of changes in prices for an asset over a certain horizon. At the same time, you don’t want to lose in the range of current prices.

Solution.Option solutions allow you to achieve break-even or a small profit within a given range of price changes.

In this case:Oil futures.

Current price 71.00. The forecast period is 3 months. The break-even range is 59.70 and above. If you just buy futures, the break-even range is 71.00 and above.

There is a forecast of levels for the day and the likelihood of their achievement. It is not clear what is the best way to work out this forecast.

Solution.Use of so-called Event contracts on CME, which represent binary options. These are fixed bets with fixed maximum profits and losses.

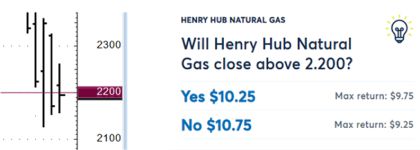

Natural Gas Futures.

Forecast: Futures will not close below 2.200 today. Such a contract is purchased and $10.75 is paid. The maximum payout under the contract is $20.00. And if the market closes above 2,200, the contract will pay out $20.00, which means $9.25 in profit (20.00 received minus $10.75 paid).

There is a forecast of changes in prices for an asset over a certain horizon. There is a desire to work out the situation by purchasing an option. Profit on the expiration date is realized only if the asset closes above (if a call is purchased) or below (if a put is purchased) the option strike. And you will need to deduct the premium paid.

Solution.The use of option combinations that allow you not to lose paid premiums in the range from current prices to the strike price. The trade-off is increased losses when prices move from current levels in the opposite direction to the forecast.

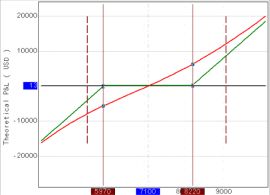

Gold Futures.

Forecast: Futures will rise. You can buy a call with a strike of 2060 at a price of 21.50. Moreover, on the expiration date, profitability will be achieved only at a level above 2081.50. Below these levels there will be a loss.

By adding several other options, you can get the following configuration: The price at which losses begin is moved below 1990.00. Trade-off - losses increase below 1990.00 compared to the limited losses of 21.50 points in the situation of just buying a call.

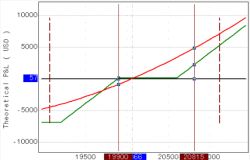

There is a position that is not developing according to plan - it is unprofitable. The position would happily be closed at breakeven, but the market has moved relatively far from the breakeven price. Often traders try to “fight back” using the so-called “averaging”: an additional purchase of an asset in the case of a long losing position or an additional sale of an asset in the case of a short losing position. Thereby bringing the break-even price closer. The problem is that the risk increases in the event of further unfavorable price movements.

Solution.Use of option combinations that allow you to move break-even price closer to current market prices. At the same time, the risk in the event of further unfavorable price movements does not increase.

Gold futures.

A long position was opened at 2050.00 (red circle). An option combination has been added at the price (green circle). Which made it possible to reduce the breakeven price to 2022.10 on the options expiration date without increasing the downside risk. Compromise - there is no profit potential above the price of 2022.10.

There is a forecast of the price level for entering a position. But the price may not reach there.

Solution.An option is sold with a strike at the level of the price entry into the position. If the price is outside the strike price on the expiration date, the option is exercised into the futures and a resulting futures position is obtained. At the same time, the opening price was improved by the amount of the option premium received. If the price does not reach the strike level, the premium received from selling the option is retained. Compromise - if the price “moved” beyond the strike and then returned on the expiration date, the option will not be exercised and there will be no futures position.

Sugar futures.

When prices are in the green rectangle, an upward trend is identified. The entry point is determined at the level of the blue rectangle. A put is sold with a strike at the level of the blue rectangle (1700). If on the expiration date the price was below 1700, the put would be executed on the futures and a long position would be opened (futures purchased) at 1700. In this case, the purchase price would be improved by the amount of the premium received from the sale of the put. In the real situation, the market did not reach the strike levels. The only profit was from the put premium. It’s not so offensive compared to the situation when there would be an order to buy futures at the level of 1700. It is also possible for the price to go below the strike and then return above the strike on the option expiration date. In this case, there will be no position in the futures, and only the premium will be earned.

There are statistical characteristics of the underlying asset (futures). Current characteristics differ from average values. The intention is to try to make money on the current market situation.

Solution.Using options on the underlying asset, a strategy for exploiting the statistical characteristics of the market is built.

The average daily price range for the last month exceeds the daily ranges for the last two days. Short-term options are purchased, which can bring profit if the daily price range increases.

There is a wide range of options strategies that must be managed dynamically and which can be tailored to the specific needs of the trader/investor.

You need sufficient experience with option portfolios and a deep understanding of the properties of options in order to implement option strategies over time. Only highly qualified specialists can guarantee high-quality execution of such strategies.

There is a long-term investment strategy, including one implemented through futures. Tactical dynamic sales of options on these futures are possible in order to receive option premiums as possible additional income.

Solution.An individual strategy using options is being developed.

Historically, options on some asset classes, especially equity indices, have been overpriced. This implies a possible advantage to selling volatility. But there are subtleties and nuances.

Solution.An individual strategy using options is being developed.

Once a position has been initiated, your view of the market may change.

Solution.Options allow you to dynamically change the composition of your portfolio to adapt to changing market views. At the same time, there is no constant need to completely close the initial portfolio. It is enough to open additional positions or change existing ones.

Hãy nêu rõ mong muốn của bạn, bao gồm cả những vấn đề phát sinh khi giao dịch và chúng tôi sẽ cố gắng cải thiện tình hình.

© 2024 Lime Trading (CY) Ltd

Lime Trading (CY) Ltd được chứng nhận và quản lý bởi Ủy ban Chứng khoán Síp theo giấy phép số 281/15 ngày 25/09/2015. Nhãn hiệu "Just2Trade" thuộc sở hữu của LimeTrading (CY) Ltd.

Số đăng ký: HE 341520

Địa chỉ: Lime Trading (CY) Ltd

Magnum Business Center, Office 4B, Spyrou Kyprianou Avenue 78

Limassol 3076, Cyprus

Tuyên bố hạn chế trách nhiệm:

Tất cả thông tin và tài liệu được đăng trên trang web của công ty chỉ có thể được sử dụng khi có sự cho phép của công ty. Để tìm hiểu thêm thông tin, hãy liên hệ với đại diện của công ty.

Giao dịch trên thị trường tài chính bao gồm rủi ro. Giá trị của các khoản đầu tư có thể vừa tăng vừa giảm và nhà đầu tư có nguy cơ mất hết số vốn đầu tư. Trong trường hợp sản phẩm có đòn bẩy, khoản lỗ có thể nhiều hơn số vốn đầu tư ban đầu. Thông tin chi tiết về rủi ro liên quan đến giao dịch trên thị trường tài chính có thể được tìm thấy trong Điều khoản chung về Cung cấp Dịch vụ Đầu tư .

E-mail: 24_support@j2t.com